Capital guaranteed investments were widely promoted in Ireland before the financial crisis, encouraging thousands of savers to put their money into so-called “100% protected” bonds.

They were marketed as safe alternatives to deposits, promising that your capital was secure while still earning returns linked to stock markets or property.

When the markets turned, many of these products failed to deliver the promised protection.

For some investors, unfortunately the fallout still affects their finances today.

A Cautionary Case

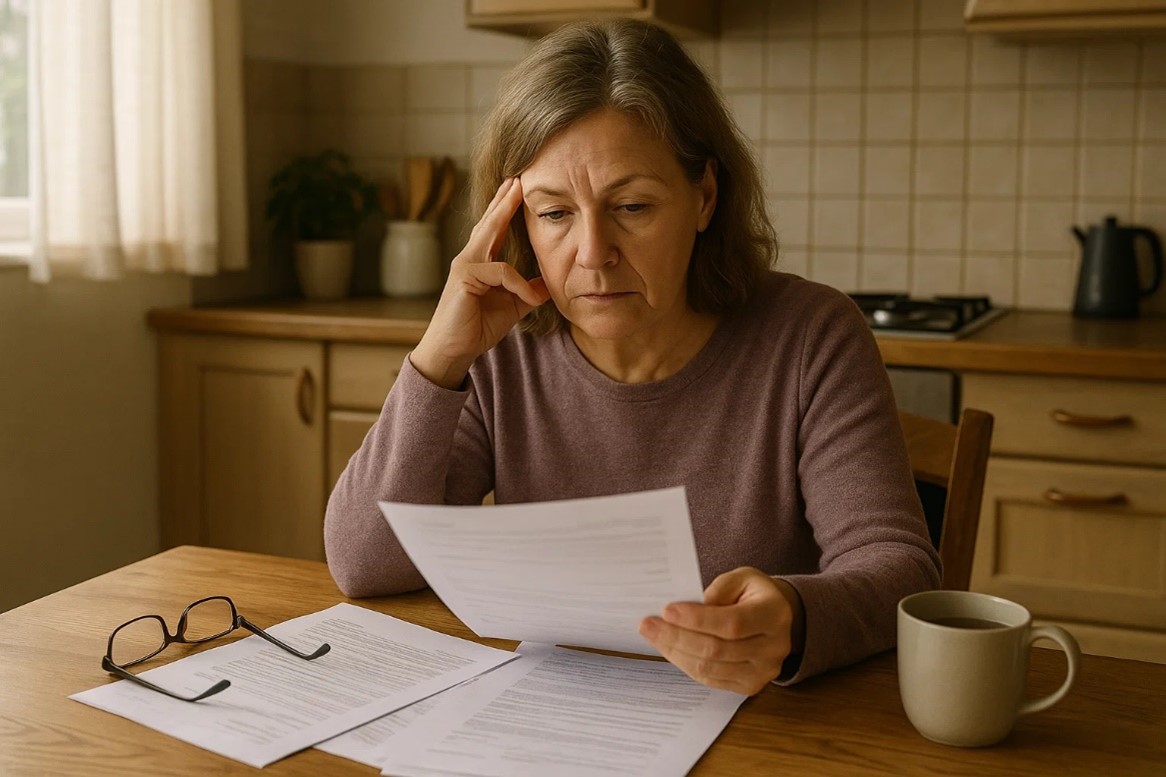

One of our clients invested a substantial sum in a bond sold through a major Irish bank in the mid-2000s.

The product brochure described it as “100 % capital protected.”

Relying on that assurance, our client also took out interest-only mortgages, expecting that the bond would mature and repay the loans in full.

When the global markets collapsed, the “guarantee” proved to be conditional, it depended on complex derivative contracts and the solvency of third parties the investor had never heard of.

The bond matured at a fraction of its value.

The mortgages remained, leaving the client in arrears and facing repossession proceedings years later.

This scenario is not unique. Similar “structured” or “capital-guaranteed” products were sold widely by several banks and intermediaries across Ireland between 2003 and 2010.

What Went Wrong

- Misleading marketing: many investors were told the bonds were as safe as deposits, when in reality the capital “guarantee” came from market instruments that could fail.

- Unsuitable advice: these complex investments were often sold to ordinary retail customers whose main goal was security, not speculation.

- Tied lending: some borrowers were advised to link mortgages or loans to the expected bond proceeds, multiplying their risk.

What the Law Says

Under the Consumer Protection Code and the MiFID Regulations, banks and advisers must:

- make sure products are suitable for the customer’s circumstances and risk appetite,

- provide clear, accurate information about potential losses, and

- avoid misleading or exaggerated claims of “guarantees.”

Where those duties were breached, investors may have claims for misrepresentation, negligent advice, or breach of statutory duty.

Complaints can also be brought to the Financial Services and Pensions Ombudsman (FSPO), which has the power to award up to €500,000 in compensation.

Why It Still Matters

Many of these investments matured during or after the crash, but their consequences, mortgage arrears, repossessions, or lost savings, continue.

With renewed focus on consumer fairness and the upcoming Consumer Protection Code 2025, mis-sold bond cases are attracting fresh attention.

If you bought a “capital-guaranteed” or “protected” bond that failed to deliver the promised return, you may still have legal or ombudsman remedies, depending on when you learned of the loss.

Contact Us

Financial products described as “safe” must truly be safe.

When customers are told their capital is guaranteed, that promise carries legal weight.

At Anthony Joyce & Co. Solicitors, we help clients recover losses from mis-sold investments and unsuitable financial advice.

We can review your investment paperwork and tell you whether you have grounds for a complaint or claim.

If you invested in a “capital guaranteed” bond that didn’t protect your money, get in touch, you may be entitled to redress.